How to Improve CIBIL Score for Small Business Funding

Getting a loan for a small business is much easier with a good CIBIL score. Lenders check this score to decide whether your business is eligible for funding. Here’s a complete, easy-to-follow guide to help improve the CIBIL score for your small business.

What Is a CIBIL Score and Why Does It Matter?

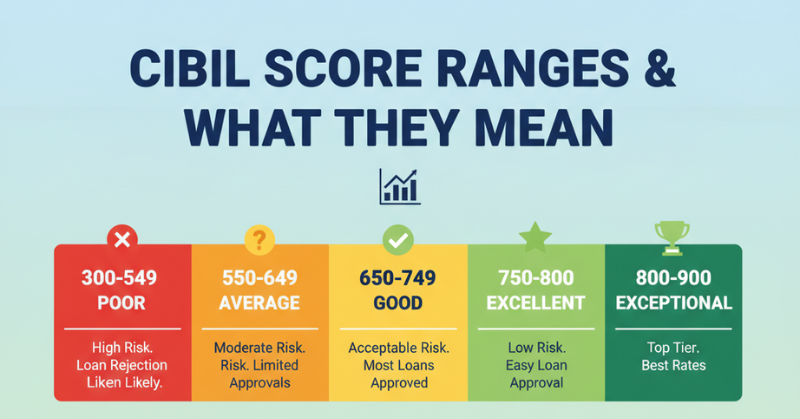

A CIBIL score is a number between 300 and 900 given to your business based on its credit history. Most banks and NBFCs look for a score above 750 for smooth loan approvals and low interest rates. If your score is below 650, getting any business loan becomes much harder, and you might face higher rates or even rejection.

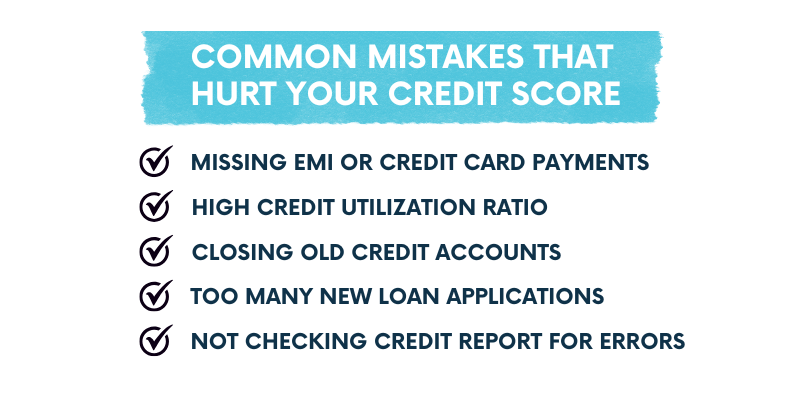

Top Reasons for a Low CIBIL Score

Understanding why CIBIL scores go down helps in knowing what to fix:

– Missing or delaying EMI and credit card payments – Using over 30% of available credit limit – Applying for several loans or credit cards at the same time – Errors in your credit report – High number of unsecured loans or defaults

Actionable Steps to Improve Your CIBIL Score

1. Always Pay EMI and Credit Card Bills on Time Set reminders or automate payments to never miss a due date. Even one missed payment can hurt your score for years.

2. Lower Your Credit Utilisation Ratio Try to use less than 30% of your total approved credit limit. For example, if your credit limit is ₹1,00,000, keep your spending under ₹30,000 each month.

3. Avoid Multiple Loan Applications at Once Applying for too many loans or credit cards in a short time signals risk to lenders and can easily drop your score.

4. Regularly Check and Correct Your Credit Report Get a free credit report once a year and look for mistakes. If you see an error, raise a dispute with CIBIL to get it corrected quickly.

5. Maintain a Healthy Credit Mix A good mix of secured (like car or home loans) and unsecured loans (like credit cards) is better than having only one type.

6. Clear All Outstanding Dues Immediately If you have any overdue amounts, clear them right away to rebuild a healthy credit record.

7. Add a Co-Signer With a Strong Credit Profile Including a guarantor with an excellent CIBIL score can help you qualify for loans and improve business credit faster.

How Long Does It Take to Improve a CIBIL Score?

With consistent efforts—timely payments, lower debts, and accurate reporting—it usually takes between three and six months to see a noticeable improvement in your score. Some changes, like correcting an error or clearing old debts, can show results within a month.

Pro Tips for Small Businesses

– Always pay at least the full amount due, not just the minimum – Avoid closing old accounts with good repayment records—they help your score – Don’t co-sign others’ debts unless you fully trust the person – Use business loans to build credit history, but repay regularly

Final Thoughts

Improving your business’s CIBIL score is one of the best ways to unlock better funding options, lower interest rates, and a stronger reputation with lenders. By following these simple, actionable steps, small businesses can build a solid credit profile, increase loan eligibility, and fuel business growth.